APLD (Follow-up) - The shady truth about APLD's potato business

Wes Cummins claims that he sold his potato business to Applied Plasma to "provide cashflow". Bankruptcy filings say otherwise

*By continuing to read this article you agree to the disclaimer at the bottom of this page.

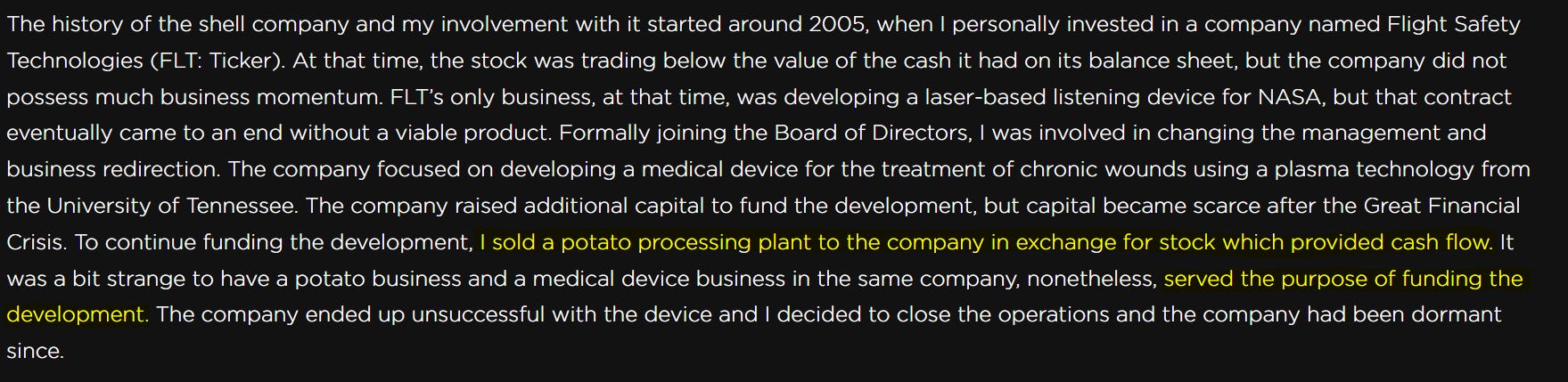

Last week, Applied Digital released a strange article on their twitter labelled “from potatoes to AI.” If you haven’t read the article – read it now before continuing with this post, or you won’t understand the context of what you’re about to read. The important paragraph is this one.

It indeed seemed a bit odd that he would give away his cashflow positive business during the GFC in return for more equity in a failing business. So I went through the old SEC filings of the shell and later bankruptcy filings of one Wes’ potato businesses to get to the truth. The potato business in question is called Cummins Family Produce (CFP) and the shell that he sold it to is called Flight Safety Technologies (FST). Here I outlay what really happened.

TLDR: here’s the truth

The “potato processing plant” that Wes sold to the company was actually loss-making, had a negative working capital position with no significant fixed assets and - without an injection of capital or immediate improvement in losses - appeared headed for insolvency within 12 months.

Wes “sold” the business to the shell in return for 65% equity. In return, the company gave an ‘assumption of obligations’ for a ~$210k promissory note that Wes Cummins personally owed to Stearns Bank. There were no hard assets included in the CFP transaction as security, as Wes had retained the equipment and land within a different private company called Cummings Family Holdings (CFH) that he owned and leased back to CFP.

CFP eventually fell into arrears, causing CFH to declare Chapter 12 bankruptcy in 2013. The bankruptcy filings show that, despite expectations of generating $700-900k, it only had positive cashflow in one year (12mo to May ‘10) of ~$72k - barely 10% of projections. In the following three years, instead of generating cashflow to fund development as Wes claims, it actually generated negative $2.2m in cashflow.

As FTS was so desperate for cash at the time of the transcation, they were not able to afford a “third party evaluation or fairness opinion.” After the transaction closed, FTS noted that CFP was previously “engaged in several significant transactions amongst its shareholders and other related parties that may not have been at arms-length” and that historical financial statements of the acquired business “would not be indicative of the operations of the ongoing business” that they acquired. It further stated that had they been able to conduct an audit of the business’s historic financial statements, “potential adjustments to the amounts included” in the unaudited statements may have come to the company’s attention. Such a comment would suggest that the company was mislead about the true economics of the business. In the end, they were right - the economics going forward were terrible.

The risk section would even state that CFP needed to raise cash for working capital in the fiscal 4th quarter. The company would go on to raise money later in 2009, ~9 months after the transaction, through none other than Wes’ employer at the time - B Riley Securities. Doesn’t anybody else see the irony in the fact that Wes’ firm profitted from raising money for FTS to plug a hole in its balance sheet caused by CFP, which was supposed to prevent them from needing to raise capital!

From the company’s last 10-Q before delisting and bankruptcy filings, we know that Cummins Family Produce produced significant negative cashflow in 9 months ended Feb 2009, as well as fiscal years ended May 2011, 2012 and 2013. In fiscal 2010, it eeked out a $72k cash inflow. Eventually, it appears that CFP fell into arrears, which caused CFH to declare bankruptcy. In the filing documents from 2013, CFH had a $500k receivable from CFP.

Ultimately, I’m sure that some will say I’m being cynical. Of course Wes was doing a good thing by providing this development company, of which he was a board member, access to cashflow - and that the company would have made $700-900k in free cashflow if not for some *insert generic business execution error/external factor here*. And I guess you can never prove that wasn’t the case.

But there is no such thing as a free lunch. I think it’s hard to explain the hole in the balance sheet and poor cashflow performance of the business immediately preceeding and following the transaction as an accidental act of misfortune.

To me, Wes has displayed a track-record of deceiving investors.

For those that want the details, keep reading.

Details

A long time ago, before APLD was applied digital, it was an OTC listed company in aerospace-related product development. Though details are not particularly important, all of the company’s revenue came from grants.

In September 2005, a proxy filing shows that Bryant Riley was a beneficial owner (>10%) through a number of investment fund holdings tied to Riley Investment Management. Bryant Riley is the founder and current CEO of B Riley Financial. Wes Cummins was working at B Riley at the time. Then, in 2007, he was appointed to the board of Directors, which was likely linked to B Riley’s stake. Wes Cummins claims that he was involved through a personal investment – this may have also been the case, but I haven’t been able to verify that he owned any stock before he joined the board.

In late 2008, the company released an 8-k that it completed a license agreement to buy some patents – this was the plasma technology that Wes referenced in the article. Buried in the release was that their proposal to the FAA for more funding for the aerospace business was rejected. With the grants gone, in the wake of the GFC, funding dried up and the company was in serious trouble.

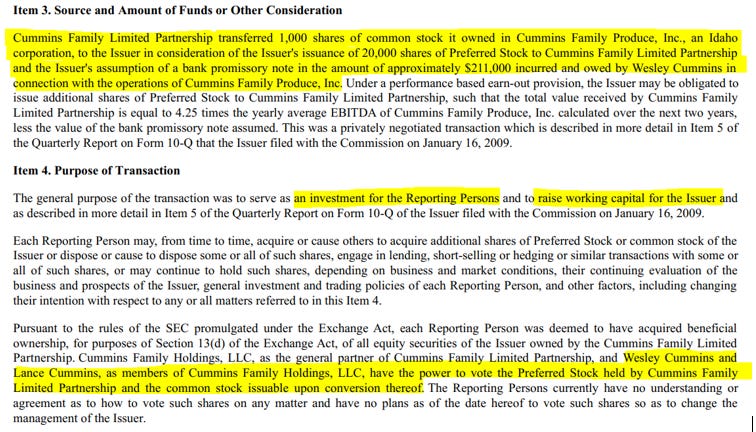

In early 2009, Wes Cummins appears on a 13-D filing with a 65% beneficial interest through a company called Cummins Family Limited Partnership. The below snippet explains the transaction.

Effectively, Wesley Cummins and his family member Lance traded their shares in CFP for a 65% stake in Flight Safety Technologies. Reason given: it was an investment for Cummins Family Holdings, and to “raise working capital” for the issuer. Further explanation comes in the next 10-Q filing.

Flight Safety Technologies bought it for its cashflow to help fund the Plasma Products Business. See below:

It was also noted that the company was only founded in 2008, and that an independent evaluation of the acquisition was not conducted.

It was effectively a fancy way to do an equity raise – give away equity for a cash-generating business. But something doesn’t add up here…

Why would Wes give away his business, capable of doing $700-900k in free cashflow, for a 65% equity stake in a failing development company? Well, probably because the company wasn’t doing so well. In the following 10-Q, we get some more financial information on CFP.

In fact, CFP’s financial position was rather precarious indeed. In 9months to Feb 28, 2009, the company lost nearly $350k. The balance sheet also had negative working capital – it had ~$1.25m in current assets against $1.6m in total liabilities, of which ~$1.5m were due in the next 12 months. There was only ~$50k of fixed assets on the balance sheet, as the agreement was only for the operating business and not the land/facility, which was retained by a different business owned by Wes and Lance and leased back to CFP. CFP was effectively insolvent and losing money. Without an injection of capital or imminent improvement in profits, it was headed for the drain.

Actually, the company even admitted this in the risk section of the 10-Q. See below, where it lists “failure to raise additional working capital projected to be needed in our fiscal 4th quarter.” The company - which was bought for cashflow - needed to raise cash. Sometimes you just have to laugh.

There’s more.

The past financials show that in the fiscal 2008 year, the company managed to eek out a profit of $85k – still a far cry from the $700-900k that management believed the company was capable of doing. To make matters worse, buried in the notes is the following comment from the company. The last line is most interesting.

It’s a bit vague, but it seems that due to inability to conduct a proper audit on the acquisition, it did not come to the company’s attention that there were significant transactions amongst the Cummins Family Produce’s shareholders and other related-parties that ‘may not have been at arms-length’. We also know, from the notes, that the majority (80%) of the company’s payables are due to two entities – Southern Slope Inc. and Black Rock Ag, which are controlled by Wes Cummins and his family members, respectively. Southern Slope and Black Rock were farms that sold potatoes to CFP, which would then package them and sell to retailers. Black Rock still exists today and is run by Wes’ family members. Southern Slope doesn’t seem to exist anymore.

During the CFP transaction, the company silmultaneously entered into a lease agreement with another holding company owned by Wes Cummins. So it is possible that the rent and price of potato-purchasing were not struck at arms-length prices in prior statements, or omitted from the financials. Not sure and not worth speculating.

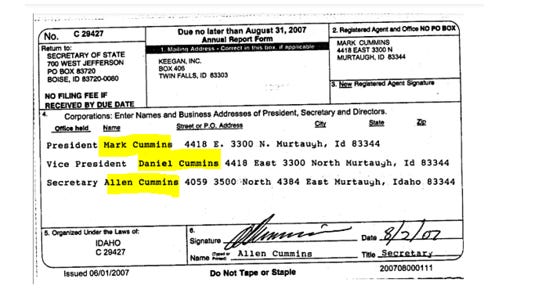

According to Idaho UCC filings, the address was previously registered to a company called Keegan Inc., and the last filing was made in August 2007 by Mark Cummins. The UCC filings also show that the Cummins family owned the facility since ~2003, when it was transferred over from Bob Keegan, who I believe to be the founder of the business.

So we know that the ‘family’ in question, accused by the company of engaging in such transactions that ‘may not have been at arms-length’, was indeed the Cummins family.

The significance of this is not malfeasance on behalf of the Cummins family, but the fact that Wes must have known what the true economics of the facility were. It had been owned by his family since ~2003, and he had been in charge for at least ~6months before selling it to Flight Safety Technologies. Either he knew, or just couldn’t understand the financials of the business he was in charge of. I find it hard to believe that he didn’t know - maybe he just wasn’t aware that his business was losing money.

I’ll let others draw their own conclusions, but it would seem to me to imply that the economics of the business were misrepresented by Wes.

But it keeps going.

It wasn’t just that CFP was losing money and had a hole in its balance sheet. Wes Cummins was also personally liable for a debt to Stearns bank tune of ~$210k as is laid out in the purchase agreement, detailed in the 13-D filing. In connection with the transaction, the company assumed all of his obligations.

So, perhaps the motive to sell the potato business to Flight Safety Technologies was to rid himself of his debt-ladden, effectively insolvent operation.

In-fact, Cummins Family Holdings – the company which owned all the machinery and land which was leased to Cummins Family Produce – went bankrupt a few years later. This was also majority owned by Wes Cummins. In the bankruptcy filings, we can see that it went bankrupt because, unsurprisingly, Cummins Family Produce (the company he sold) fell into arrears and stopped paying the lease.

The company eeked out a small cash inflow in 12-months to May 2010, and then fell into significant losses again until it eventually stopped paying rent. The 700-900k of free cashflow was never even remotely close to being reached.

And then the cherry on top.

Later in 2009, the company would go on to raise money as predicted. The raise would be done by B Riley - the firm that Wes Cummins was working for at the time. Presumably, at least part of this offering was used to plug the hole in CFP’s balance sheet that they alluded to in the risk section. It then raised money again in 2011 twice (here and here).

Does anybody else not see the irony in this? Wes sold CFP to FTS so that they wouldn’t need to raise capital. Instead, they ended up needing to raise capital for CFP. And to top it all off, Wes’ firm earned fees raising them the money.

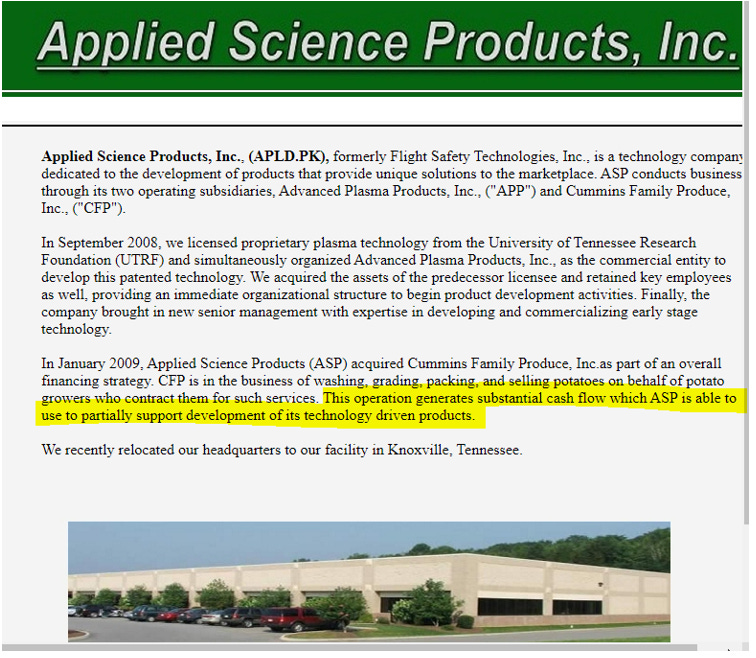

Going back through the Wayback Machine, we can see that the company was still promoting itself on its website in December 2009, despite having been delisted. It claimed that CFP was generating “substantial cashflows” which was partially used to develop its technology driven products. It did not mention that their recent fundraising round was to add working capital to CFP. Of course, we now know from bankruptcy filings that CFP indeed was not generating significant cashflows, and in the future it would go on to do quite the opposite.

Advanced Plasma Products actually had a bit of success. It raised some more money in early and late 2011 and then relied on grants for a few years. The company was officially dissolved in 2019.

As for Wes’ assets. The packaging facility is now owned by Eagle Eye Produce - it’s unclear when that happened. Who operates it is unclear, but it seems that Eagle Eye both own and operate the facility.

Conclusion

Take away what you want.

My interpretation from the above events is a deliberate attempt by Wes Cummins to deceive investors and rid himself of a failing business + personal debts. Wes Cummins has, time-and-time again, missed lofty forecasts at APLD, such as those made in the 2021 and 2022 investor deck. Read some of the snips below/check the forecasts in the deck, then go see how those worked out. With this track-record of missing targets/misleading investors, how can people honestly trust that the 2023 forecasts are anything more than a figment of imagination?

More to come.

Disclaimer

You agree that use of Guasty Winds Management LLC's (“GWR”) research is at your own risk. In no event will you hold GW Research or any affiliated party liable for any direct or indirect trading losses caused by any information on this site. You further agree to do your own research and due diligence before making any investment decision with respect to securities covered herein. You represent to GWR that you have sufficient investment sophistication to critically assess the information, analysis and opinion on this site. You further agree that you will not communicate the contents of this report to any other person unless that person has agreed to be bound by these same Terms of Service. If you download or receive the contents of this report as an agent for any other person, you are binding your principal to these same Terms of Service. You agree and acknowledge that the materials, opinions and contents available on this website (or any other GWR social media platform, including Twitter, Instagram, Snapchat or Facebook), are not investment recommendations and are indeed not recommendations of any kind.

This website contains solely our investment opinions. We are invested behind our investment opinions. Material on this website and all statements contained therein are solely the opinion of Guasty Winds Management, LLC, and are not statements of fact. Our opinions are held in good faith, and we have based them upon publicly available evidence collected and analyzed, which we set out in our research reports to support our opinions. We conduct research and analysis based on public information in a manner that any person could have done if they had been interested in doing so. You can publicly access any piece of evidence cited in on our website or that we relied on to write our repots. Think critically about our reports and do your own homework before making any investment decisions.

You should assume that as of the publication date of our reports and research, GWR (possibly along with or through our members, partners, affiliates, employees, and/or consultants) along with our clients and/or investors and/or their clients and/or investors has an investment position in all stocks (and/or options, swaps, and other derivatives related to the stock) and bonds covered therein (either long or short depending on our investment opinion), and therefore stands to realize significant gains in the event that the price of changes in conjunction with our investment opinion. We intend to continue transacting in the securities of issuers covered on this site for an indefinite period after our first report, and we may be long, short, or neutral at any time hereafter regardless of our initial investment opinion.

Nothing contained on this website is an offer to sell or a solicitation of an offer to buy any security, nor shall GWR offer, sell or buy any security to or from any person through this site or reports on this site. Guasty Winds Management, LLC is not registered as an investment advisor in any jurisdiction. The content and materials contained on this website are provided for information purposes only and nothing contained therein is investment advice nor should it be construed as such. Prior to making any investment or hiring any investment manager you should consult with professional financial, legal and tax advisors to assist in due diligence as may be appropriate and determining the appropriateness of the risk associated with a particular investment. Users of the GWwebsite and any material contained therein shall not use the site at any time for any purpose that is unlawful or prohibited and shall comply with any applicable local, state, national or international laws or regulations when using the site.

If you are in the United Kingdom, you confirm that you are accessing research and materials as or on behalf of: (a) an investment professional falling within Article 19 of the Financial Services and Markets Act 2000 (Financial Promotion) Order 2005 (the “FPO”); or (b) high net worth entity falling within Article 49 of the FPO.

Our research and reports express solely our opinions, which we have based upon generally available information, field research, inferences and deductions through our due diligence and analytical process. To the best of our ability and belief, all information contained herein is accurate and reliable, and has been obtained from public sources we believe to be accurate and reliable, and who are not insiders or connected persons of the stock covered herein or who may otherwise owe any fiduciary duty or duty of confidentiality to the issuer. However, such information is presented “as is,” without warranty of any kind, whether express or implied. GWR makes no representation, express or implied, as to the accuracy, timeliness, or completeness of any such information or with regard to the results to be obtained from its use. All expressions of opinion are subject to change without notice, and GWR does not undertake to update or supplement any reports or any of the information, analysis and opinion contained in them.

You agree that the information on this website is copyrighted, and you therefore agree not to distribute this information (whether the downloaded file, copies / images / reproductions, or the link to these files) in any manner other than by providing the following link:

http://www.gw-research.com

or a sublink to a specific report. If you have obtained a GWR research report in any manner other than by download from such links, you may not read such research without going to that link and agreeing to the Terms of Service.

Any links from our site or our reports are provided for viewer convenience. GWR is not associated or affiliated with any linked sites. Independent providers have prepared all information accessible through these links.