Carlisle (CSL-US) 1Q23 Update

Earnings were a little soft due to higher destock than anticipated. Cyclical headwinds likely to persist for a few quarters.

Carlisle’s earnings came in a little soft in the quarter, driven mostly by a greater magnitude of de-stock than first anticipated and some weather-related delays. In addition, the company lowered guidance for the year for CCM with a hit to both margins and volumes. I was already below guidance on margins for this year but I was too high on sales, and the deleverage has caused margins to come in <30% for 2023.

I’ve lowered my EPS from $20.80 to $18.90. The stock is trading at $207 after-market, which puts it at ~11x updated EPS.

It’s going to be a bumpy couple of quarters as we are somewhat earlyish in a downgrade cycle. My position isn’t full, I’ve been buying down from $260. Mistake to move so early into a downgrade cycle probably but on a medium-term view I think it’s too attractive to ignore. Will buy a bit more here and be buying more aggressively if it gets under $200.

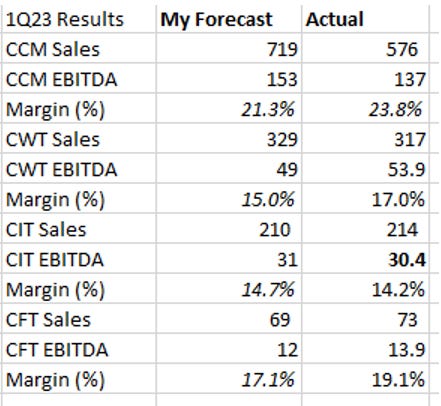

Overview of numbers

Here’s a high-level overview of the numbers v.s. what I had modelled. Not sure what the street had because I don’t currently have access to a BBG. Not going to just summarize the result/call as you guys are capable of flicking through the docs yourselves and I don’t think it adds any value. 8-k and Transcript here and here. But I will add my thoughts.

CCM sales miss was the big surprise. The company called out the destock and some weather-related impacts at ~80-20% weighted towards destock. This has been happening across the whole building products industry (both resi and commercial) and is well understood, though the magnitude was a little higher than originally anticipated. Basically what happened is that when contractors couldn’t get product they started leasing warehouses and stocking up and nobody (OEMs or distributors) knew exactly how much product was out there. Contractors would never do that in normal times; 90% of the time product is delivered direct to site, so this is not an issue that the business is used to dealing with. And so I think we can forgive management for getting the forecasts wrong. Carlisle feel that they have good visibility over that now, and that whilst it will continue to drag a bit on 2Q, it should be done by mid-year.

On end-demand, the company’s channel surveys suggest that sell-through volumes remain solid with contractors and that the downgrade to sales is on the back of inventory clear-out, not end-demand. That said, it’s an uncertain time. Backlogs for re-roof remain healthy, which was the same feedback that I received back in 1Q when I did checks. New construction is obviously a big question mark and I think that management have about as much visibility on that as any of us. Some conservatism is called for with the current state of the world.

The big positive was that margins held in at ~24% given a huge (~35% YoY) volume destock. That is encouraging for two reasons. One, it shows the strength of the variable-cost nature of the business, still able to generate significant profits in weak-volume environments. Two, it is positive to see that, despite a significant volume decline, pricing held in. It’s unlikely that recent price increases pushed through will stick. In fact, commentary suggested that pricing will probably slip a bit this year as raw materials come down (which was the feedback I had in 1Q from the channel). Mgmt. has guided for flat pricing YOY, and given that there was probably 1-2% of carryover pricing, that would suggest some light declines in the backend of the year as the company starts to feel some relief on costs.

Mgmt. are confident that next year, CCM will return to 30% EBITDA margins and that the new target is for 30%+. This still stands to be proven but they’re on the right track, despite a cyclical set-back. Reminder that I had 2024e margins at 28.5% in my base case numbers.

On CWT, sales were similarly impacted by destock/weather but margins came in better than expected, which was mostly just a realization of synergies from the Henry business. Not much else to call-out there and I’m not going to bother with the other businesses, they are both producing good results.

Updating my 2023e numbers

I’ve brought down my sales forecasts for CCM to reflect the new guidance of Down HSD. The company is also expecting margins to be down 100bps instead of slightly positive. I previously had down 40bps so I’ve taken that down a bit. Reminder than I have margins falling considerably in 2024e whilst management expects 2024 to expand to 30% - my base case had always built in a few 100 points of margin degradation to ~28.5% (from 31.6% in 2022 and 30.6% in 2022e).

This lowers my 2023e EPS from $20.80 to $19.10. Outer years remain relatively unchanged but come down slightly also. At the post-market price of $207, this still puts the stock at ~11x P/E.

Paid subs can ping me for an updated model.

Summary

It’s just a quarter and it is the weakest quarter of the year. The path forward is likely to be bumpy, as we already know. We could/probably will see further downgrades to numbers in 2023/24. Margins/pricing are holding in as hoped thus far, which I think is the most important thing to watch for the stock. So for now, structural story is on-track and I’m holding/buying on weakness.

Appreciate the update sir!