Civeo Corp (CVEO-US)

FY27 could be a meaningful inflection year

Disclaimer: Not financial advice, do your own research, I may own, buy or sell stocks mentioned in this article at any time, etc.

I recently bought a position in Civeo. Life as a public company has been nothing short of misery for Civeo shareholders. However, I believe that the company is on the cusp of a potentially meaningful inflection in earnings and free cashflow. Recent engagement from a well known activist has pushed management towards significant capital returns. I also believe that their Australian assets are of under-appreciated quality worthy of more attention.

Civeo is in a cyclical business and so there are a range of outcomes and the risk is higher than things I would typically own. However, if things go well, I believe the stock could be a 2-3x over a 1-2 year period.

Introduction and Brief Investment Thesis

Civeo is a workforce accommodations company that provides permanent villages, temporary lodging and integrated services (catering, housekeeping, etc.) to workers in remote resource extraction regions. They have two businesses: Canada and Australia.

The Australian business predominately serves the Bowen Basin – the world’s premier high-quality Coking Coal region. The Canadian business predominately serves the Oil Sands regions in Alberta. In addition, they have ~2,500 rooms of mobile camp assets in Canada, similar to those owned by Target Hospitality (TH-US). These are currently sitting idle.

Life as a public company for Civeo has been nothing short of a disaster. The company was spun off from Oil States International in May 2014 at the peak of the Oil Sands and Met Coal booms. The company was severely over-earning in both regions with occupations at 100% and day-rates well above historic norms. The spin-off was supposed to be structured as a REIT, but the IRS denied it REIT status. The stock fell 50% in one-day, and then proceeded to decline ~95% from its peak. Profits fell by ~80%.

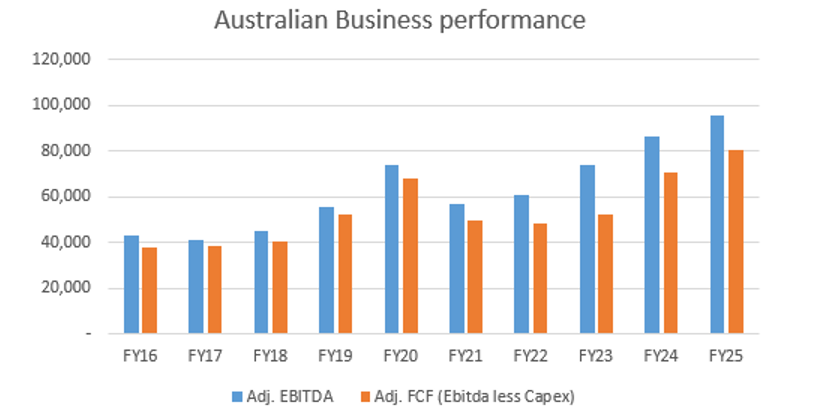

From 2016-2023, the underlying business was mostly doing fine, except for some volatility around Covid. The Australian business exhibited strong growth whilst the Canadian business had some volatility with oil but still generated plenty of cash. From FY16 to FY24, the company generated ~$700m of unlevered Free Cashflow, or ~$75m/year on average. A majority of that went towards paying interest and de-levering the balance sheet from 4.5x to <1x with a measly ~$70m ear-marked for investor returns. Historic underlying cashflows from Civeo have been very robust.

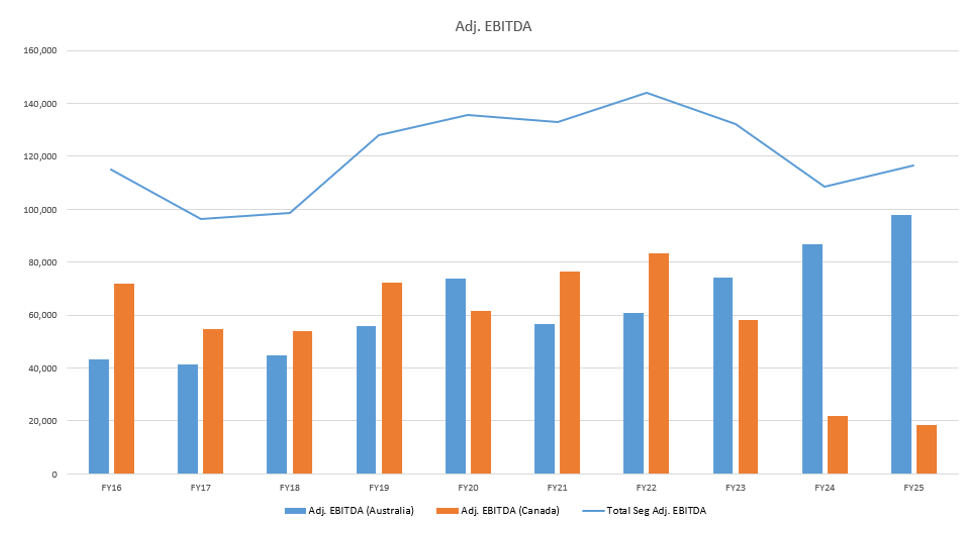

Since 2023, as one will see from the chart below, Civeo has become a tale of two businesses. Australia has continued to grow and perform extremely well whilst the wheels have fallen off the Canadian business.

Below I will explain the situation in a bit more detail, starting with the woes in the Canadian business.

Canada’s Woes

There are two parts to the Canadian business and both have been a thorn in Civeo’s side. First is the lodging assets in the Oil Sands region. The long-short of the situation is that Canadian oil sands operators have been on a multi-year journey to reduce their cost structures. A big part of that has been reducing labor intensity on site - particularly FIFO workforce. These really started to take place in 2023 and hit the company hard in 2024/25. The company’s EBITDA collapsed over this period from $80m to just ~$20m in FY24 and FY25.

In early 2025, the Canadian business tipped into losses and Civeo made the decision to restructure the business. They cut overhead meaningfully and closed multiple lodges with poor occupancy. They’ve effectively right-sized the business for the new reality of Oil Sands. Whilst it’s possible that the region could show strong occupancy growth, the major oil sands companies have favored share buybacks over new investment, and Civeo doesn’t expect a meaningful uptick.

The good news is that this should be a trough level. Occupancy seems to have stabilized in 2H25. In fact, the company is expecting that FY26 may even be a slight uptick from FY25. Customers have cut labor so meaningfully already that Civeo struggles to see how they could possibly go much lower - of course anything could happen. The Oil Sands companies have also done a great job lowering their break-evens to low $30s and even into the high-$20s, meaning that they’re much more resilient to $55-60 WTI than they used to be, and one wouldn’t expect meaningful business disruption at that level outside of a material negative oil shock - current occupancy levels are ~consistent with $55 oil in late 2025.

I estimate that the business should be able to generate ~$22-25m in EBITDA in FY26 and build from that level if things improve. Canada is not the key earnings driver, but stabilization in this business is key as it was previously loss-making.

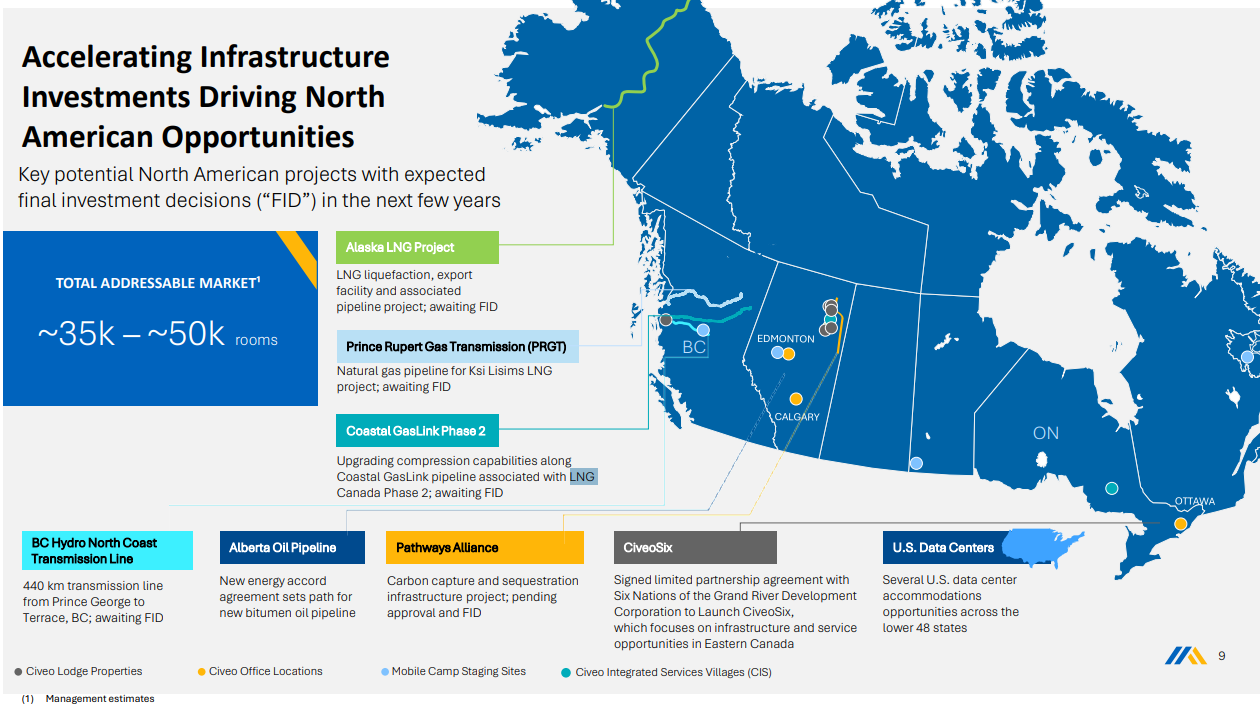

The other part of the Canadian business is the mobile camp assets. These are deployed to remote projects which are large but temporary in nature. For example, new pipelines. Civeo has ~2,500 readily deployable camps sitting idle in Canada. These were previously deployed into two pipeline projects: TMX and Coastal Gas. Both projects finished ~22/23 but the camps weren’t redeployed - there just weren’t any large infrastrcuture projects to redploy to.

The outlook here seems to be warming up. There are currently a large handful of large pipeline, LNG and infrastructure-related projects in Canada that are awaiting FID with an enormous amount of addressable rooms. The company is hopeful that these projects will achieve FID this year, after which a decision on the rooms will be made shortly after. Civeo has one of the largest idle fleets of mobile accomodations in North America and should be well-positioned to serve at least a portion of this demand.

I’m no expert here but I’ve done a little digging on these and it seems likely that we’ll get some FIDs in 2026. Coastal Gaslink Phase 2 is expected by its owners to take FID in 2026. Civeo supported Phase 1 of this project and is likely well positioned to support phase 2. PRGT is sexpected to achieve FID in late 2026 and has been selected by the federal government for fast-tracking. FID is also expected this year for the BC Hydro transmission line where early works have already taken place.

In addition, there’s also the Data Center piece that I’ve written about in the past. Target Hospitality recently won a 1,500 bed project and has discussed a 15,000 bed pipeline. Civeo is seeing a similar thing noting that the sales folks are as busy as they’ve ever been. Given the sizes of these projects, Civeo only really needs to win 2 or 3 projects to soak up its capacity.

As I understand it, at the peak in FY21/22, the Mobile Camp assets generated ~$25-30m in Gross Profit (effectively, EBITDA) on an average deployed room count of ~1,600. They currently have 2,500 rooms sitting idle and another 1,000 rooms that are attached to lodges in Canada that could be mobilized with a small amount of capex.

Hence, with ~2,500 to 3,500 rooms to deploy, the assets could generate an incremental $30-60m of EBITDA for Civeo. The company has significant NOLs in the US and Canada and deminimis capital would be required for the first 2,500 (small amount for the next 1,000), meaning that EBITDA should largely drop straight down to FCF. For a company that will do ~$35-40m of FCF this year, this would provide an enormous windfall.

The company is not in control of project FIDs, however they’ve mentioned that revenue generation from the mobile assets could come as early as late 2026 and full run-rate in FY27. I would expect that we will hear announcements in the coming 1-2 quarters about projects here. I don’t believe that the stock is currently pricing in any success in re-contracting these assets.

Put together, with just the 2,500 rooms deployed, I estimate that the Canadian business could generate ~$70m of adj. EBITDA in FY27.

The Aussie Cash Cow

The Australian Assets includes two businesses: Owned Villages and Integrated Services. Owned Villages consists of rooms that are owned and operated by Civeo. Integrated Services consists of services provided for assets that are not owned by Civeo (i.e. managing captive assets on behalf of a mining company). The services business is growing well, but ~80% of Australia’s EBITDA today is still provided by the owned villages. The owned assets are predominately located in the Bowen Basin of Queensland. The Bowen is predominately a Met Coal region.

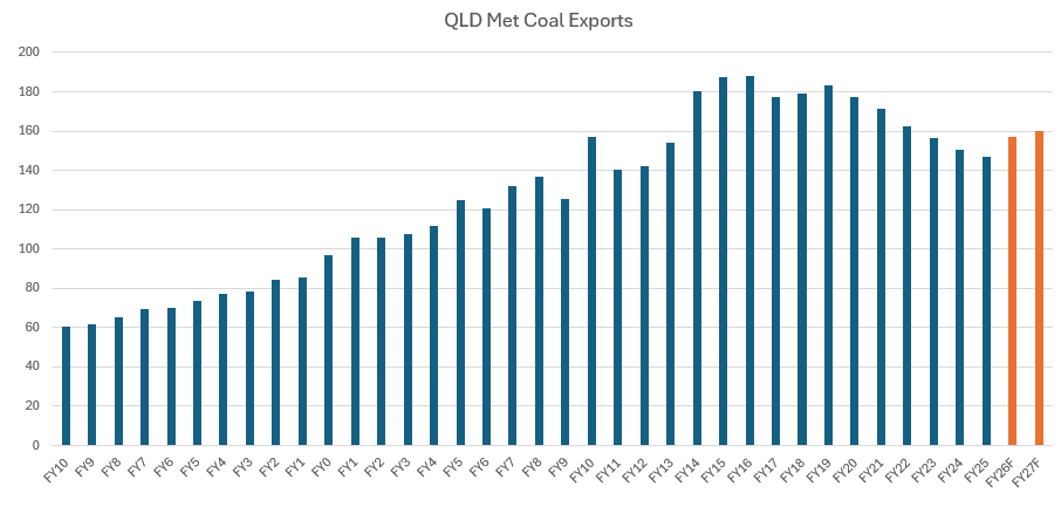

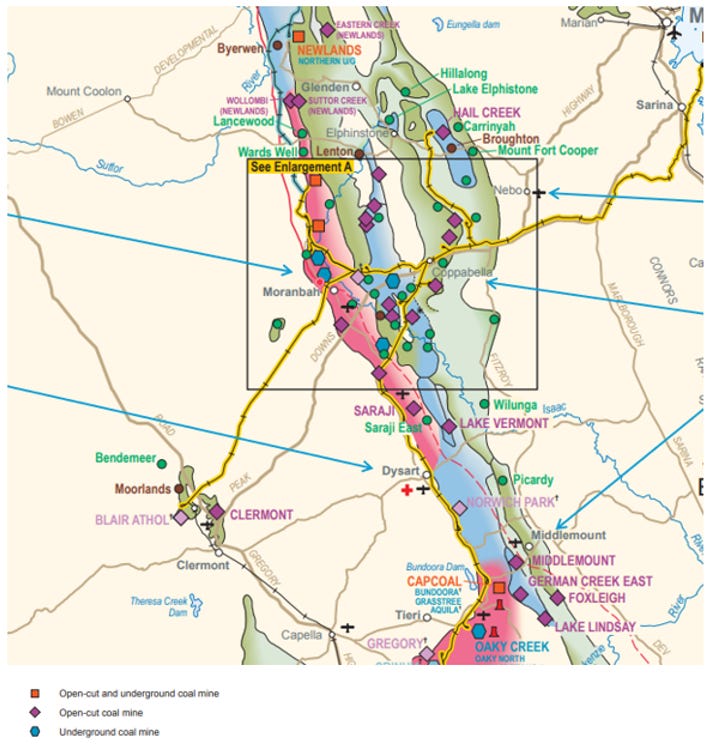

The Bowen Basin is located in central Queensland. It hosts ~48 active coal mines and produces ~half of the world’s seaborne supply of Met Coal. It’s an enormous region, covering ~60,000 square kilometres (larger than Tasmania) and its mines are scattered across vast, sparsely populated landscapes ~150-300kms inshore. The closest major regional city is Mackay – a coastal hub about 200kms East.

Bowen is blessed by remarkable geological characteristics. The basin’s Permian-age coal seams were deposited in conditions that produced thick, laterally extensive measures with excellent coking characteristics. It is known for its high-quality coal – low ash, low sulphur and high vitrinite. Bowen Basin coking coals command premium pricing on global markets, with brands like Peak Downs, Goonyella, and Saraji setting benchmark prices.

Given the quality of assets, the region has historically been relatively stable outside of the 2010-13 boom/bust period. Production and exports have declined recently largely driven by a decline in demand from China, partly offset by an increase in demand from India. Met Coal is predominately used in steel production, so China’s slowdown/global weakness in construction/automotive production has impacted seaborne demand in recent years. Exports are forecast to rebound in FY26 and FY27.

It’s worth noting that the fundamentals of the Bowen Basin are quite a bit different to Abathasca oil sands. Oil Sands produces a small fraction of the world’s oil and was generally considered to be high cost. The Bowen Basin produces 50% of the world’s seaborne Met Coal exports and is home to the highest quality Met Coal in the world. Whilst it is still susceptible to impacts from commodity prices, the Bowen Basin is more critical to Met Coal than Abathasca Oil Sands are to Oil. It should be more stable as a result.

That’s visible when observing the company’s sound operating history throughout multiple commodity price cycles.

Over time, employment in the region has been relatively stable-to-growing, and the number of avaialable beds has remained relatively flattish. The fundamentals are strong for workforce accommodation in the basin.

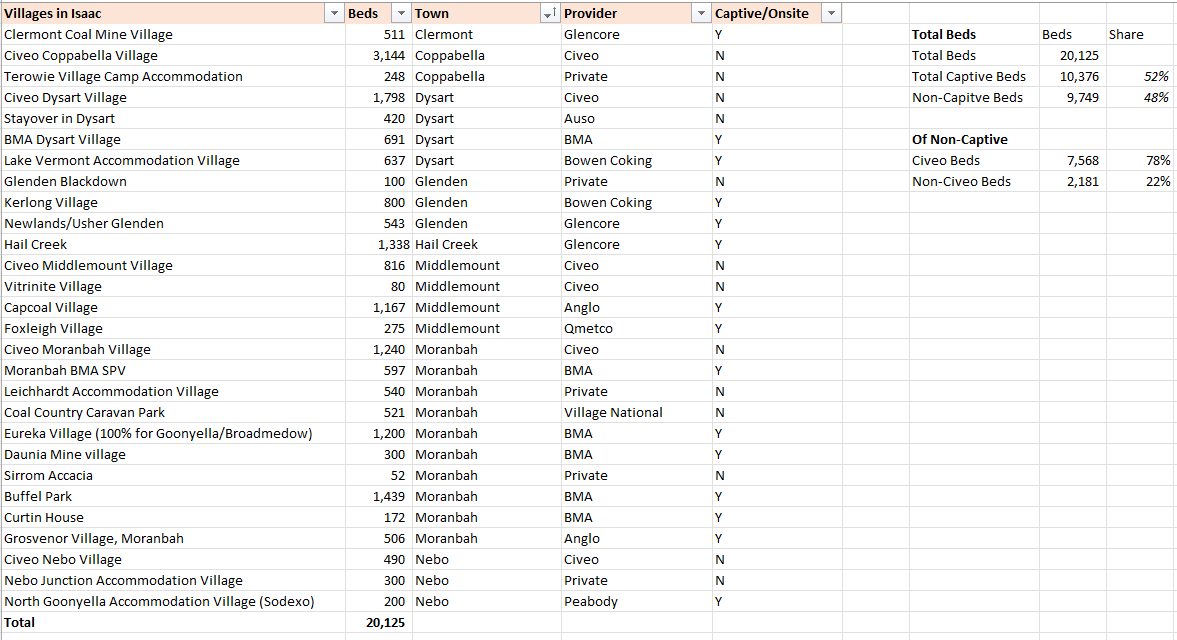

~50% of beds are owned by mining companies themselves with ~50% by private companies like Civeo. I estimate that in the Isaac LGA (main LGA within the Basin), Civeo has ~80% of non-captive beds. In other words, they have a very strong competitive position.

From a high-level, Civeo’s Isaac villages are well-situated in the major cities of Isaac, nestled between large operating mines and dozens of proven deposits. Copabella, Moranbah and Nebo are well-situated in Northern Isaac, each surrounded by a handful of active mines. The Middlemount assets are similarly well positioned to service a cluster of open-cut mines in Southern Isaac. The Dysart village acts as an overflow for assets between Moranbah and Middlemount, as well as serves Lake Vermont and Saraji.

According to management and confirmed by 3rd party reports, Civeo’s Northern Isaac accommodations (~55% of its total legacy room count) are at capacity and have been for some time. From a late 2024 economic needs assessment (report).

“Based on conversations between Pacific National and Civeo, the Civeo Nebo Village, Coppabella and Moranbah all are currently at capacity with no additional availability for Pacific National employees in the foreseeable future”

And from the company’s earnings call: “3 of our Bowen Basin villages continue to be effectively operating at full capacity, and we’re seeing strong occupancy across the remainder of our owned village portfolio.”

All of this is to say that the Basin’s long-term fundamentals are sound and that the supply picture is favorable. However, it is not immune from commodity weakness. In FY25, the Met Coal price weakened and occupancy took a hit in 2H25 for Civeo, particularly in 4Q25.

The company has guided to lower occupancy in FY26. However, Met Coal prices have recently recovered from their FY25 lows. On the 4Q25, Civeo seemed confident that levels would stabilize at these levels and potentially improve if Met Coal prices were to hang in at this level. Of course this could change at any given moment.

Though fluctuations will impact EBITDA for the Aussie business over time, it seems to be a fundamentally sound set of assets capable of generating significant cashflows through the cycle and on more structurally sound footing that the Oil Sands assets given the position of the underlying Basin relative to global commodity demand/supply.

Unpacking FY26 Guidance and upside

The company guided to $85-90m in EBITDA in FY26 which would amount to ~$30-40m of FCF depending on capex.

I think that there could be upside in FY26 guidance if things continue as they are. The key assumptions in the company’s guidance from their call were:

Stabilization in Canada with flat to slightly up occupancy.

Weakness in Australia, with consolidated occupancy roughly flattish YoY (would amount to ~MSD% organic decline in occupancy YoY).

No contribution from the mobile camp assets.

With these assumptions, I get towards the high end of the EBITDA range. I have modelled flat occupancy in Canada and taken a slightly more bleak view on the Australian business with organic occupancy -HSD% YoY. This gets me to ~$87m of EBITDA on constant currency rates.

However, the company’s average AUD/USD exchange rate in FY25 was $0.645. Though the company didn’t explicitly comment on the exchange rate in their guide, my modelling suggests that they’ve baked in no impact from FX. The AUD/USD currently sits at ~$0.71, or ~8% higher than their average for last year. This should provide a tailwind from 1Q26 but especially in 2Q26. If the exchange rate holds at this level, I estimate a ~$7-8m tailwind to EBITDA guidance in FY26.

Altogether, I’d expect EBITDA of ~$95m and FCF of ~$43m in FY26, putting the stock at ~7x FCF. The company has already repurchased 500k shares in 1Q26 (~$13m, or ~4% of S/O) and has another authorization. Going forward, they’ve comitted to at least 75% of cash returned to shareholders. I would expected most of that cash to be used for buybacks with some modest develeraging.

In FY27, with a little fortune, things could really inflect higher. If occupancy were to recover to FY25 levels in Australia (which should be consistent with met coal prices at current levels of ~$220-240) and the CIS business continues to march towards its $500m AUD revenue goal, I estimate that the Australian business could do ~$115m of EBITDA in FY27. As discussed, if the 2,500 mobile camp rooms get deployed, then the Canadian business could do ~$70m in EBITDA. With ~$26m in overheads, that would get Civeo to a consolidated EBITDA of ~$160m and ~$100m of FCF.

Share Count should be ~10m by the end of the year, which would be a market cap of ~$280m, putting the stock at <3x forward FCF. Even at a modest 6-8x FCF multiple, there’s significant upside to the stock at current levels.

Loads can go wrong for Civeo but you don’t have to believe much for this scenario to come true. The stock is on a single-digit FCF entry multiple with a commitment to repurchase stock. There’s risk but I like the R/R at $28.

He’s back

Great piece on Civeo. Hopefully they'll make some great tuck-in acquisitions in the future, that could increase EBITDA and strengthen their market position even further.