SMRT - Accounting vs. Reality

SMRT underlying business continues to deteriorate whilst accounting numbers paint a rosy picture.

SmartRent’s 2Q was a bit of a head-scratcher. The significant growth in sales from 1Q didn’t carryover into 2Q, with top-line decelerating from ~74% YoY in Q1 to 26% YoY in 2Q. Trends of key KPIs suggest deterioration in the underlying business is continuing and in fact worsening, as we have seen from industry peers recently. The exact cause of such is unclear given management’s hesitance to provide clear commentary. It would appear that a mix of macro headwinds and destocking are the culprit.

The company also announced that it signed a deal with ADI for distribution. Though the details on the call/press release were vague, some may have noticed from the 8-k that there was a clause in the agreement for inventory repurchase. Essentially, it provides an avenue for the company to artificially boost its freecashflow short-term to hit its target. I will go into it in more detail below.

Things to discuss

Quick review of earnings

Review of underlying KPI trends

Distribution agreement with ADI will allow the company to temporarily increase its FCF. Underlying economics of the business will remain unchanged.

Earnings Review

Total revenue continued to grow YoY at quite a considerable clip - 26% YoY - despite having materially decelerated from 1Q. SaaS revenue grew at a modest 8% YoY and professional services revenue grew at 10%. Hardware revenue grew at 33%, largely assisted by the accounting changes. Hardware shipments were up 17% YoY in the quarter, with the remainder being ARPU. The notes to the accounts stated that the ARPU increase was “primarily driven by hardware revenue recognized on the shipment of distinct Hub Devices during the three months ended June 30, 2023.”

This change had a positive impact on gross profit, as expected. Hub Amortization began to decline slightly in Hosted Services revenue, creating a mix shift towards SaaS that assisted gross margins. The inclusion of hub devices in hardware also aided hardware gross margins to increase to 21%. At the same time, gross margins for services deteriorated likely caused by wage inflation and lower utiliziation of labour on lower installments.

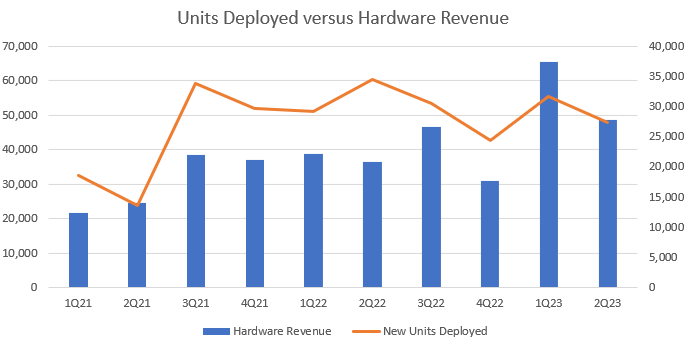

For contrast, this is how hardware revenue compares to Hub Installations. As deployments have trended down, revenues have sky-rocketed.

Total gross profit for the quarter was ~$10m. Operating expenses were ~$22m despite significant YoY layoffs. Even after the revenue recognition change, the company is quite some ways away from achieving GaaP EBIT positive. Excluding ~$3m of SBC and ~$1.3m of D&A, the company still generated negative adjusted EBITDA of ~$6.5 (when also excluding ~$1m of severance and acquisition related expenses).

Reviewing underlying KPIs

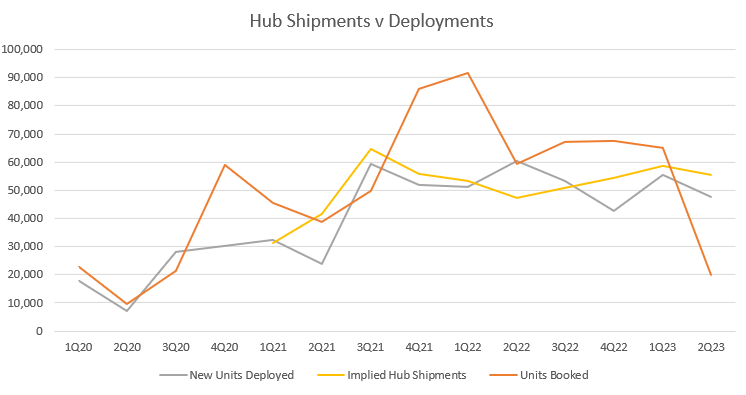

There has been a big divergence between shipments, deployments and bookings this year. Below is a chart that shows the three key KPIs. We only get sipments on a quarterly basis from 1Q21.

The big shock from the result was the big drop-off in units booked. The company doesn’t give a backlog, so it is hard to know for sure the magnitude of work that has been prior booked but not performed. Generally with a steadily growing business, you will see backlog the largest, flowing into higher shipments which flows into higher deployments all with a slight lag. From 1Q20 to 2Q23, the company has cumulatively booked 703k units, shipped 619k and deployed 561k. However, this year the trend has reversed. In 2H23, it has shipped 120k units, deployed 103k units and booked 85k units.

The company explained this on the call as follows:

It is possible and in fact likely that at least part of the decline in units booked is due to destocking. We’ve seen this across the building products space this year as supply constraints in 2021/22 caused double-ordering and restocking which is unwinding as things have normalised. But Lucas denied any macro weakness.

On the last call, the company noted that as of 1Q it was substantially free from supply chain constraints, suggesting that through 1H23 it should have been able to deploy at a higher rate. If bookings were falling because the company simply booked so much work that it needs to get through it all before customers sign more orders (as the company suggests), I’d have expected that easing supply chain constraints would have led to higher deployments to meet such elevated backlog. That hasn’t, in fact, been the case. Deployments were down -7.5% YoY in 1H23 over 1H22, when supply constraints were considerable. In 2Q23 specifically, they were down 21% YoY - a clear deceleration from 1Q.

In contrast, shipments increased by 13% YoY in 1H23 and 17% YoY in 2Q23. It is odd but not entirely unusual to see shipments increasing whilst deployments decrease. In one of the company’s early investor presentations, it noted that units are generally deployed the quarter after being booked. So I would assume that the timing between shipping and deployment is also less than 1 quarter, but it may have blown out recently with supply constraints. Remember, SMRT is mostly doing refurb. projects and not new-builds and mostly installing its own units, so it doesn’t make sense to have product piling up at the job site and the company should have good visibility into its own labour availability. I’m not suggesting that shipments are being pushed into the channel - in-fact, if you look at the chart from before, you can see that shipments lagged in 2022 due to inventory constraints, so it might simply be catch-up.

In any case, it is odd to see that shipments have grown to catch-up after supply constraints, but deployments have been stagnant and in-fact down YoY. All the while, bookings have fallen off a cliff. It just doesn’t square with the company’s commentary that the backlog is so high that customers are pushing out new orders.

Elsewhere, the company’s competitors have been discussing weaker volumes and elevated inventories across the industry due to over-ordering at the same time as falling volumes. The following is comment from Resideo - the owner of ADI distribution and one of the largest smart home manufacturers in the country - about the current inventory situation.

In the press release, they discussed weaker volumes.

We won’t properly know until the next quarter as to what really drove the large decline in bookings in the quarter, and it is to be seen if that number bounces back quickly. It seems likely that the company is facing cyclical headwinds and customers seem to be hitting pause, at least to a certain extent.

What is clear is that deployments are not growing, despite supply chain headwinds subsiding. Deployments are the single biggest driver of the business. Accounting tricks have created significant sales growth in 2023, but deployments have barely budged on a quarterly basis since 3Q21 2021.

Expect a temporary artifical boost to FCF

In early August, the company signed a distribution partnership with ADI. The release was a bit vague. ADI had already been supplying the company with Resideo thermostats, but this agreement would expand to more product lines.

In the 8-k, we get a little bit more info:

The latter two duties refer to ADI selling the company Resideo product (exclusive) and 3rd party product (could be Nest, Ring, whoever). The first point is the most interesting. The company and ADI entered an inventory-buyback agreement. The terms are laid out below.

On the call, Lucas explains the relationship as follows:

Effectively, ADI will become an inventory wharehousing facility for SmartRent. Currently, it has $60m of inventory on the balance sheet (representing ~6 months of hardware sales). ADI will be buying inventory which is currently owned by SmartRent to sell back to SmartRent under the distribution agreement.

My understanding is that this should be treated as a financing agreement. What’s unique about this type of agreement (as opposed to borrowing from a revolver to finance inventories) is the recognition cashflows. Under this agreement, cashflow will be recorded in the operating line (via changes in inventory) as opposed to the financing line. This means that it can include this increase in its free cashflow calculation. Effectively, it’s a fancy way of borrowing money and counting it in FCF.

Why does that matter? It isn’t real FCF. The will experience a temporary boost as it shifts its inventory to the distributor, and then this boost will go away. Yes, the company will be come more capital efficient, but with $190m of dormant cash sitting on the balance sheet, I’d argue that capital efficiency is not exactly the company’s main issue.

ADI will also stock and manage inventory on behalf of SMRT effectively as a 3PL provider; according to their call, they are already doing this currently with Fedex. There probably are benefits to using ADI’s specific service, given that they are a dedicated building products distributor. That said, money isn’t free. The company can still have 3PL (as it does now) and maintain ownership of inventory. There will be a cost to moving the inventory off their balance sheet, and it doesn’t make sense that the company is financing inventory whilst also hoarding cash if not to try inflate FCF.

I will be watching how they account for this agreement like a hawk. I am NOT accusing the company of anything, but such repurchase agreements are common-place for accounting abuses such as channel-stuffing. Again, not saying that the company is doing this - they are not. But I will be watching closely to make sure that these inventories sales are not being booked as revenue.

What am I to do with this stock?

I shorted a bit at the open on earnings day and I could close that whenever. I was not expecting for such a drastic deterioration in deployments or bookings and the stock opened down just 3% which I thought was way too generous. I will most probably not (unless I change my mind) hold the short into the next print, as I believe that the company is going to use the ADI relationship to show positive FCF. As evidenced by the stock’s recent performance post the 1Q rev-recognition change, despite obviously deteriorating underlying business, I don’t think that the analyst community is looking far beyond headline numbers. And I don’t want to be on the wrong side of a positive surprise.

I’m watching this one like a hawk. 2024 consensus is calling for a 35% increase in sales to $350m. With the current trend in bookings and and deployments, overlayed by a deteriorating macro environment and industry which has way too much inventory, I am at this point very sceptical that the company is going to hit that target, absent some miraculous re-acceleration in the business.

The sugar hit from revenue recognition will wear-off in 4Q23, and revenue trends for 2024 will begin to emulate underlying deployment trends. 1Q24 is going to be a massive bar for the company. I will likely play this into the 4Q print on dissapointing forward guidance, but that’s a long way away. Stay tuned.