The Security I like Best

ProPetro Holdings (PUMP-US): Data Center Power Play on a trough 15% FCF yield

Disclaimer: Not investment advice, DYOR, views my own, etc.

Ticker: PUMP-US

Stock Price: $11.26

PF S/O (post-raise): 121.5m

Market Cap: $1.37bn

ADV: ~$30-40m

PF Net Cash (post-raise): $105m

Enterprise Value: $1,260m

FCF Yield: 15%

Overview

ProPetro is an oilfield services company. Their legacy business is tied to completions largely in the Permian; specifically, pressure pumping. It’s a nasty business - capital intensive, competitive and highly cyclical. The stock’s historic multiple of 4-5x EBITDA reflects that reality. It does, however, throw off a lot of cash.

In late 2024, ProPetro entered the on-site power generation business through the formation of a new subsidiary: ProPwr. ProPwr provides onsite generation through small turbines (20-50MW packages) and reciprocating engines (~5-15MW packages) for the Oil and Gas and Data Center industries. In effect, they bring power to your site and run a small (or sometimes large) mobile power plant on medium or long-term contracts.

The economics and growth potential in ProPwr are distinct and far superior to the legacy completions business. I forsee significant growth in ProPwr. I believe that ProPwr alone could be worth >$30/share within 3-5 years. The current market cap is incorporating almost zero value for the ProPwr business today despite its phenomenal success over the last 12months. My 2-year base case is ~$35.

I have an enormous portion of my net worth invested in this stock. Details below.

The Behind-the-meter (BTM) power opportunity

It’s not news to anyone that the grid is struggling to connect required large loads on requested timelines. This hasn’t stopped the data center industry from building as quickly as possible. The key problem is that data centers are either (1) following construction timelines that run ahead of the grid, or (2) built for loads well in excess of what the Utility can realistically deliver in the short/medium-term. Many data centers today are being started without line of site on the utility or a plan to connect to the grid at all. The significance of this is that data centers need to find power to get their data centers energized before the grid is available.

Elon put it most elegantly himself earlier this year:

“The limiting factor for AI deployment is fundamentally electrical power. We’re seeing the rate of AI chip production increase exponentially, but the rate of electricity being brought online is negligible. It’s clear that we’re very soon, maybe even later this year, we’ll be producing more chips than we can turn on.”

— Elon Musk, World Economic Forum, January 2026

“Between now and then, the constraint for server-side compute, concentrated compute, will be electricity. My guess is that people start getting to the point where they can’t turn the chips on for large clusters towards the end of this year. The chips are going to be piling up and won’t be able to be turned on. So how are you going to turn the chips on? Magical power sources? Magical electricity fairies?"

— Elon Musk, Dwarkesh Podcast, February 2026

The grid continues to move at a glacial pace, and whilst most investors assume that the grid will “catch-up”, by all accounts it appears to be falling further and further behind. This has caused an urgency in the industry to bypass the grid entirely and build onsite power plants.

Realistic options for onsite power are largely limited to two: Nuclear or Gas (Solar and Wind are ruled out due to intermittency). Nuclear is not really part of the conversation for the next decade and is also not fast, which just leaves gas. However, anyone that’s read a GEV earnings call knows that Heavy Duty Gas Turbines are heavily backlogged and EPC labor is heavily bottlenecked.

So what choice do we have? Fortunately, we do have a solution. Utilites already have a need to deploy fast emergency generation when large generators go offline due to weather damage. Their solution hss historically been to deploy a fleet of packaged mobile generators (mixture of large reciprocating gas engines and small single-cycle turbines) to plug the gap. These are basically “power plants on wheels” that can deploy fast and reliably.

Below is a picture of what these look like. It’s literally a generator on wheels which includes a mobile substation (balance of plant). Sometimes they are skid-mounted when the deployments are longer-term in nature.

There’s strong consensus amongst industry participants that a mixture of packaged reciprocating gas engines and small gas turbines will be the BTM solution of choice.

The most famous case for this solution is Elon’s Colossus cluster, which relies upon 750MW of small Cat turbines (going to 1.5GW by early 2027 and likely beyond). Solaris (SEI-US) is the vendor for this project and really was the first to prove out the concept at scale.

Why the recent fuss about BTM?

I go to a lot of Data Center Industry conferences. In mid-2025, I started noticing a significant pick-up in discussions for BTM power from industry folk. This was followed by a handful of public deal announcements from VoltaGrid, Cat, Wartsilla and ProPetro as well as private deals without public announcements that I picked up from field work.

In October, things seemed to really picked up steam. I spoke with multiple private engine OEMs at conferences that spoke of significantly extended backlogs for within the last 4-8weeks. One of them sold ~2 years of production to a single customer. Another spoke of multiple gigawatts of late-stage, firm deman. Around the same time, we also saw a capacity announcement from Cat (the industry’s largest supplier) on the back of “unprecedented demand” in early November. One private BTM provider told me at a conference that he was getting multiple calls asking for 300-400MW of capacity per day.

It’s unclear exactly what has catalyzed the mad rush for capacity. My hypothesis from extensive conversations and following the space for some time is that it was driven by a collection of the following:

Existing grid capacity seems to have been exhausted, and projects are now necessarily being started without a substation or even transmission line with the hope that it may come eventually, necessitating BTM.

Many large-scale projects were started in 2024 or 2025 which should be nearing energization in 26/27. As utilities are slipping on timelines, BTM crunch-time is coming.

The sheer scale of power demand has pushed customers to look at all possible options for power generation. Small Turbines and recips are the most proven and fastest amongst available options.

Recent legislature in ERCOT (SB6) has given Oncor the ability to “force curtailment” of load. This has necessitated BYOP. It now seems that most, if not all, projects in Texas will be built with onsite generation. Texas alone is an enormous data center market especially for large training sites.

PJM has been a little bit messier. They initially proposed mandatory curtailment in August 2025. However, stakeholders pushed back on it and they removed the mandatory concept in October. In Jan of this year, they released a new proposal that achieves a similar outcome: voluntary BYOP can achieve expedited connection and avoid curtailment. If one doesn’t BYOP, they are subject to curtailment before emergency demand response.

Utilities have generally continued to be unreliable outside of Virginia. Many DC developers are adopting the attitude of “you can’t trust the utility.” Timelines are dissapointing and being met with more scepticism.

XAI’s Grok 4.1 model was a huge success and enabled by having the largest cluster of GPUs in the world. It was a sort of real-world verification that scaling laws hold and that Coherent clusters have distinct advantages over distributed compute. It was also built in break-neck speed. A key enabler of the speed/scale of the Colossus clusters was Solaris and its BTM turbines. They have enabled Elon to scale >1GW in a matter of months.

The Chip shortage seems to have caught up but power remains a constraint (Satya comments, Elon comments, etc).

Oracle’s recently announced mega-deal with OpenAI will be powered by 2.3GW of Jenbacher reciprocating engines by a company called VoltaGrid. This has probably caused people to pay attention and perhaps a “rush” to secure capacity in recognition that megadeals are coming which could clog up the supply chain just like they did with large turbines. There’s already proof from my work that this is happening.

Who’s playing? Oil Services companies have a right to play and right to win

In much the same way that Bitcoin miners were in the right-place-right-time for large-load sites, oil services companies are in the driving seat for BYOP.

The reason is that the grid in the Permian is almost non-existent. In fact, the Permian has been facing a similar power problem as the data center industry over the last few years, albeit at much smaller scale. Historically, equipment (such as a frac pump) in the permian was powered by diesel engines. As the key E&Ps have become more concious of emissions, they’ve been moving away from diesel and towards electric powered equipment. However, the unreliability of the grid has caused E&Ps to look towards small natgas microgrids to power that electrical equipment.

Some E&Ps or pressure pumpers (such as ProPetro) have experimented with doing this themselves. However, this trend has given birth to a new business model of BTM power in the Permian. This is the use case for which VoltaGrid was created.

In addition, companies like ProPetro have a lot of experience dealing with large scale diesel and gas engines that have powered their frac fleets for many years. The heavy mechanical skills are largely transferrable to BTM and their relationship with CAT (from whom they’ve purchased over $1bn of equipment over time) is critical in securing a reliable supply of generators. In fact, one might argue that running a stationary microgrid on a clean Data Center site is easier than mobile engines in the desert out in West Texas.

The key players today in the market all started in the oil patch (Solaris, VoltaGrid, Liberty and all the private players) because they already have the product and business model to service data centers.

The big debate: A grid stop-gap or sustainable business model?

Anyone who has followed Solaris knows that the bear-case on BTM been some form of the following: Sure, Solaris is pretty profitable today, but when the grid catches up to demand, Solaris will have no business model! It’s just a stop-gap to 2030.

This was the prevailing view even ~6months ago and the investment markets (even those of us who traffic heavily in power stocks) were skeptical of BYOP, seeing it simply as a bridge-to-grid.

I have come to a very different view over the last 6 months.

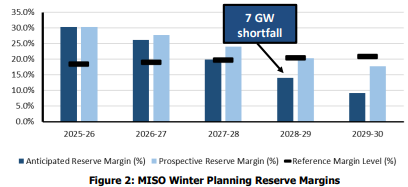

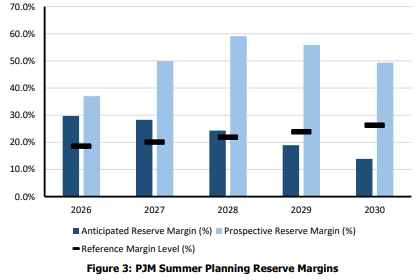

Firstly, it seems that the supply/demand gap for power is worsening and will continue to worsen as the scale of sites keeps growing. Many analysts and consultants have done estimates of power supply/demand and whilst it’s hard to model with accuracy, Morgan Stanley shows that the deficit through to 2030 continues to grow and will reach 40-50GWs by the end of the decade. It’s not hard to reach a view where this is seen as conservative. NERC’s recent reliability assement shows that PJM and MISO are facing significant power shortfalls in the short-term - i.e. this is not a 2035 problem, it’s a 2027/28 problem.

This shortfall is BYOP’s market. Overall demand is significant and will continue to grow for the foreseeable future with new sites needing onsite power even if the older ones transition to the grid.

However, where I have really changed my thinking is on this point: the assumption that data centers will rent equipment for a few years and then hand back the generators seems to be a huge a misconception. In a mad rush to scale up, why would a power-constrained data center hand back valuable power when the grid arrives instead of adding the grid to existing onsite gen? In fact, I have heard multiple anecdotes of exactly the latter happening. A VoltaGrid employee that I met at a conference noted that they’ve never had any equipment returned once it’s gone to site. He showed me a picture of a deployment in San Antonio and asked, with a brief pause and a wry smile, “do you think they’re moving those any time soon?” The CEO of a large DC operator joked with VoltaGrid after they deployed mobile turbines that “they’ll never get these back.”

Solaris’ experience with XAI has been similar. XAI originally expected to rent 80MW of turbines for 6 months whilst they waited for the utility. It then went to 400MW for 2 years and now 1.5GW for 7 years. The utility arrived with 400MW, but their demand just kept increasing. Instead of returning the power, they’ve used the grid to boost their overall power. XAI’s commitment to funding a JV with Solaris also shows their long-term belief in onsite power. It’s one of the very few examples that we can actually point to, but it’s a positive signal.

A discussion I had with a procurement person at one of the hyperscalers explained to me that their strategy is to use onsite gen to power all of their cooling loads where possible (less critical and complex loads, typically making up for 30-40% a DC’s power usage) to free up more grid power available for scaling up data halls. This also validates my view about onsite power being more permanent in nature.

It’s also true that most existing sites will continue to scale in size beyond what they initailly get from the utility. For example, someone at another Hyperscaler explained to me that maybe you asked the utility for 500MW by 2030 and bridged the gap with onsite power, but by the time that comes, you need 1GW which the utility can’t deliver until 2035, so the turbines will stay. For the foreseeable future, it’s likely that individual sites will continue to add campuses as fast as they can. It’s much easier to add a campus to an existing site than it is to build a new site and so existing sites will look to scale up where possible.

We also have recent proof from XAI that scaling existing campuses is important for model performance. Coherent training clusters are important drivers of model performance and Semi Analysis has written a lot about this.

In addition, rack densities are going to grow by a factor of 10-20x over the next 3-5 years which should lead to exponential increases in power requirements for existing sites that wish to host the newest generation of servers. Take, for example, a data hall that today only has 100kw rack densities increasing to 300kw and eventually 1MW. Without more power, this data hall will sit only 1/3 or 1/10th full as each rack is now pulling 3-10x more power. This will happen over the medium-term and put consistent upwards pressure on the power needs of existing sites. A site that finally got 300MW from the utility (or built on an existing site with power) can’t simply get another 300MW just because they got connected – they have to go to the back of the queue. BYOP should play a role in helping existing campuses continue to scale.

It’s also worth noting that this trend isn’t just about power quantity, it’s also about power quality. Large training loads pose significant challenges for grid operators as the have enromous surges and drops in power draw that occur in a matter of miliseconds and cannot be forecast by the grid operator. When we’re talking about 1GW+ clusters, these loads could make up a significant portion of the local grid operators service area, and a swing like that could interupt the frequency of the grid so meaningfully that it would bring the entire system down.

One large Data Center Operator that I spoke to who works on the Abilene project noted that one of the Stargate projects would have been ~40% of the load in that particulary electric service area. How can a grid planner possible cope with a 40% load swinging around like crazy?

This poses an issue for those wishing to power their data centers entirely from large CCGTs, also. CCGTs can only run ~80% of the time and take ~30 minutes to go from zero to full capacity. How can a CCGT cope with the load variations of training data centers? They can’t. In fact, META famously dealt with the load variations by having its chips solve for 1=0 (or some other impossible calculation) so that they would always keep working (a gigantic waste of resources) and not interrupt the grid. Microsoft does a similar thing.

Onsite generation, using batteries or intertia, can cope with these swings much better than a large scale CCGT. Most industry folk believe that Large Data Centers of the future will be connected via microgrids where small turbines can play an important role alongside more economical CCGTs or SMRs. A micro-grid like this could also build-in enough redundancy to support the grid and make back-up diesel gensets redundant. (Most people don’t appreciate that Diesel gensets are insanely expensive and almost never get used).

Onsite Gen also has another distinct adavnatage - it’s fast and scalable. Once a fleet of engines is deployed, the Data Center can scale up in a modular fashion by adding more engines and upgrading the balance of plant. It’s much easier than getting more power from the utility which would require going to the back of the queue and also timely and costly infrastructure upgrades.

Lastly, onsite gen might prove to be even cheaper than grid power in some areas and on some timesframes. The significant pushback against utilites passing transmission costs for Data Centers onto customers means that transmission upgrades are going to be borne solely by the data center operator. Inflation in equipment and labor means that building transmission today is way more expensive than in the past. Today’s power curve is extremely misrepresentative of where grid prices are going, and when one compares the gargantuan costs to upgrade transmission to serve these new loads, onsite gen is likely to be much closer to parity with the grid on a 5-10year view.

For example, if you can sign a 10-year PPA with a BTM provider at a 15% premium to the grid today, it might still be NPV positive considering where grid power prices will be towards the latter end of that contract.

I am aware of atleast one deployment in Texas where onsite gas gen was cheaper than the grid (advantaged access to cheap gas + unique situation where the utility tarrif was super high, but it’s an illustrative datapoint of where we could be headed).

My view is that there will be multiple forms of onsite power. First, there will be true bridge power - short-term contracts where the power needs are truly of an emergency nature and returned shortly after. But there will also be more permanent deployments of onsite power which are effectively acting as scalable onsite power plants. The latter will come with long-term, take-or-pay contracts. And demand for the latter seems to be on the cusp of entering a boom era.

Settling the “Stop-Gap” debate: Long-Term Contracts are here

6 months ago, my hypothesis was that we’d see contract tenors extend. Today, you don’t really need to take my word for it. Long-term contracts are here.

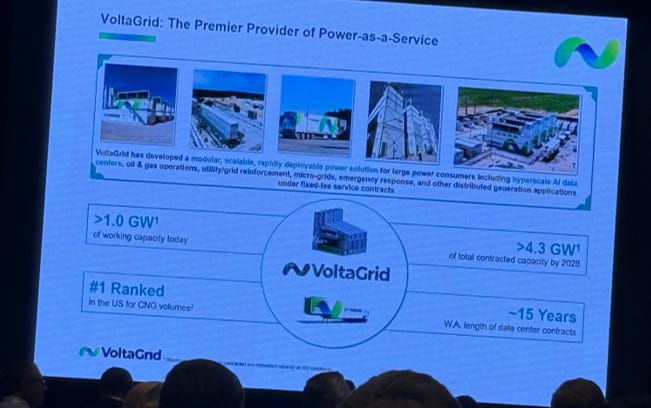

Late last year I was at an industry conference and VoltaGrid gave a presentation. I nearly spat my coffee out when I saw the bottom right textbox of the following presentation slide:

15 years… 15 years?! Yes. 15 years. That’s about the same length as a data center contract.

It suddenly dawned on me that there’s a huge disconnect between what the investment markets perceive to be “stop-gap solutions” and what industry folks are viewing as long-term deployments. At the time, the public markets had not yet any proof that these long-term deployments were going to happen as VoltaGrid is a private company and Solaris’ longest term contract with XAI was ~7-8 years (investors remained sceptical about the repeatability of such a deal).

Since my initial work last year, we’ve seen further proof of where the market is going:

In November, Williams announced a 10-year Data Center contract with 2x5 year options.

In February, Williams announced that both of their data center contracts saw the tenor extended to 12.5 years.

“And we've showed the team has done a great job of extending the contract terms on 2 of the projects, but we're seeing additional momentum for that going even further over time.”

- Chad J. Zamarin, CEO of Williams, Feb 2026

In February 2026, Solaris announced a 10-year contract with an unnamed Hyperscaler with a 5-year option to extend.

In January/February 2026, Liberty announced a 1GW framework agreement with Vantage Data Centers and an additional 330MW deal with an unnamed customer in Texas. Liberty noted that these are “long-duration” but didn’t explicitly clarify the term.

I strongly believe (based on conversations with private players) that current deals in the market are being negotiated with long-term tenors such as these above, and I believe that we will see a flurry of long-term contracts singed this year which validate my view that BTM power is not a stop-gap but rather a critical long-term power solution. This supports my view on multiples for companies in the space (which I will address later).

Let’s talk about ProPetro

ProPwr was officially launched in December 2024 when ProPetro hired Travis Simmering and Dave Bosco from Dynamis Power. Dynamis is a leading microgrid company operating in the Permian and has >500MW under contract (mostly in the Permian), so these guys are intimately familiar with running and scaling a BTM power business.

ProPwr originally targeted the oil and gas market. In early 2025, it became clear that the data center market would be a big opportunity for them. In May, ProPwr signed their first deal for 80MW in the Permian and in late October they signed their first Hyperscale data center deal for 60MW, which shocked the market. Whilst Permian power will continue to grow, the emerging data center opportunity is significant if they can execute.

On the most recent call (Feb 18), Sam acknowledged that Data Center will soon overtake Oil and Gas in importance:

“Moreover, we are seeing a growing number of inquiries from potential data center and industrial clients. Over time, we anticipate these opportunities occupy a higher share of our overall capacity, driven by both their larger load needs and longer-term strategic commitment. - Sam Sledge, Pro Petro CEO

The ProPwr business currently consists of ~240MW of contracted power. 60MW of the total is with a Hyperscale data center customer whilst the rest is in the Permian. The oil and gas business is out on 10-year tenors whilst the DC business is on an undisclosed “long-term” tenor.

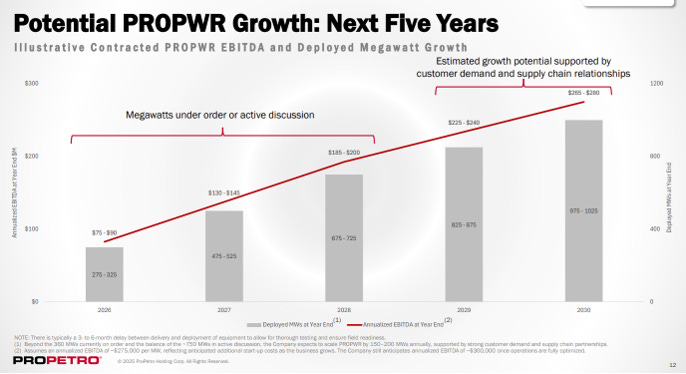

The company’s plan is for 750MW of contracted power by the end of 2027 and 1GW by the end of 2030. Given that they finished 2025 with 230MW under contract, the 1GW by 2030 target is probably conservative. My base case is that they will end 2030 with at least 1.5GW of contracted power. Even at their current run-rate of ~230MW/year, they will surpass their 2030 target by ~400MW. In fact, the company has recently increased its 2027 target from 475-525MW to 550MW and the 2028 target from 675-725 to 750MW. I expect that the below chart may also be updated shortly.

It’s important to put in context how relatively little power 1GW is in the context of a data center. Recent deals from SEI, WMB and LBRT have ranged from ~350-500MW for a single data center. Sam also acknowledged on the call that a chunky data center deal would push their targets way up. I believe that the recent capital raise was to prime the balance sheet for a larger deal.

“That said, to the upside of that, some of these non-oil and gas data center, industrial type projects can be much bigger and chunkier in nature. So one of those can potentially change that time line and that mix very significantly if we're able to capitalize on one of those opportunities soon.”- Sam Sledge, Pro Petro CEO

ProPetro has taken a little bit of a different approach than LBRT and SEI. LBRT and SEI’s approach has been to order a very significant amount of equipment in order to have capacity for the “Mega Deals” - GW+ scale stuff. ProPetro has been a little bit slower and methodical in its apporach, instead preferring to pick off smaller contracts and get equipment deployed into the field faster. I do think that recent comments from the company + the recent capital raise indicate a willingness to push for larger contracts.

For the “why not just own WMB or SEI” askers, I say that I do own both of those stocks. However, I see a much more attractive R/R for ProPetro and it is my top pick amongst the small handful of companies pursuing this opportunity. This is why:

Team and Ability to Execute

Travis and Dave built Dynamis largely from scratch to >500MW under contract. They were both in the engine OEM business at Baker Hughes and MTU, respectively, before getting into the mobile gen business. Granted, they know exactly how to build a mobile power business and they’ve assembled a strong team including a handful of ex-employees and ex-competitors. Feedback on the team from competitors (including from Solaris and other private competitors) has been positive.

Travis hit the ground running in his first 12 months. He has taken the business from an idea on paper to 230MWs within 1 year, including a contract with a Hyperscale data center – an elusive target even for some of his competitors that have been in the business for multiple years.

ProPwr is earlier in its life than Solaris and though they’ve secured their first contract, they still need to prove to customers that they can execute. Their original contract is a great starting point but it is admittedly small.

With this 60MW contract, they’ve got a chance to perform and cement their position in the data center market just like Solaris did with XAI. There’s more power at this existing site and at other sites for this customer, and Travis is confident that they’ll win plenty more business if they can execute on this contract. For context, Solaris started with an 80MW contract from XAI in May 2024 which will be >1GW by the end of 2025. Solaris’ team was similarly acquired from a private company with Permian experience.

The hyperscale contract will go live from 1Q26 after an extensive engineering period. I think they have a real good shot at executing but only time can tell. If they can do a good job for their first customer, I see no reason that ProPwr couldn’t scale at a similar pace to Solaris and smash through its 2030 1GW target.

I also like management. I’ve travelled to meet the ProPwr teams and the C-Suite in Midland and Houston. Sam and Caleb are straight-shooters and err on the conservative side. They understand that this is a significant opportunity for the company but have erred on the side of conservatism with managing street expectations (relative to peers such as LBRT who’ve promised huge deals).

Travis and Dave are also great. They’re power experts and they know what they’re doing. They’re also straight-shooters and don’t get caught up in the hype. Exectution is priority #1, 2 and 3. Travis put to me that “demand is the least of his concerns” as it pertains to hitting their 1GW target - execution is everything.

2. Highly asymmetric valuation

Below, I’ve provided a very simple upside analysis for the stock depending on how much capacity we can deploy in the future. I want to stress three points.

The 240MW scenario (what we’ve currently contracted) gets us to a stock price above the current level. That is to say: the recent move in the stock price has not even reflected what we’ve contracted let alone upside from here.

There’s very significant upside in the stock if ProPetro extends its Data Center business. 3-4x is my base case. I think a 10x over 5-8 years is totally within the realm of possibility if ProPwr exectues flawlessly.

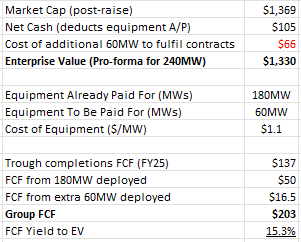

Downside is heavily protected by (1) a net cash balance sheet and (2) 15% starting FCF yield to EV based on just the contracts that we’ve signed today and trough permian conditions. Completions FCF was $100m in 4Q25 - it was an extroadinary quarter (low capex, good market conditions, some WC unwind), but FCF could be very siginificantly higher than $150m/year if we get $70+ WTI. Things are already improving in the Permian and FY26 should be better than FY25.

Before I do the SOTP, I want to show the FCF Yield calculation. I don’t use the company’s FCF for completions because it excludes the lease costs. Instead, I calculate my own as EBITDA less Capex (cpy. has significant NOLs so I don’t subtract Tax, but you can if you want).

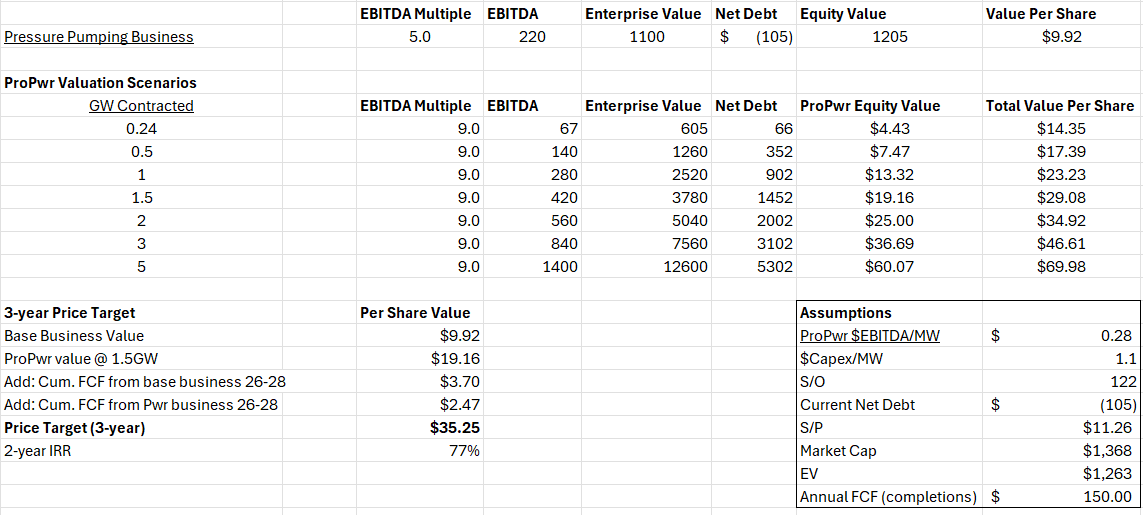

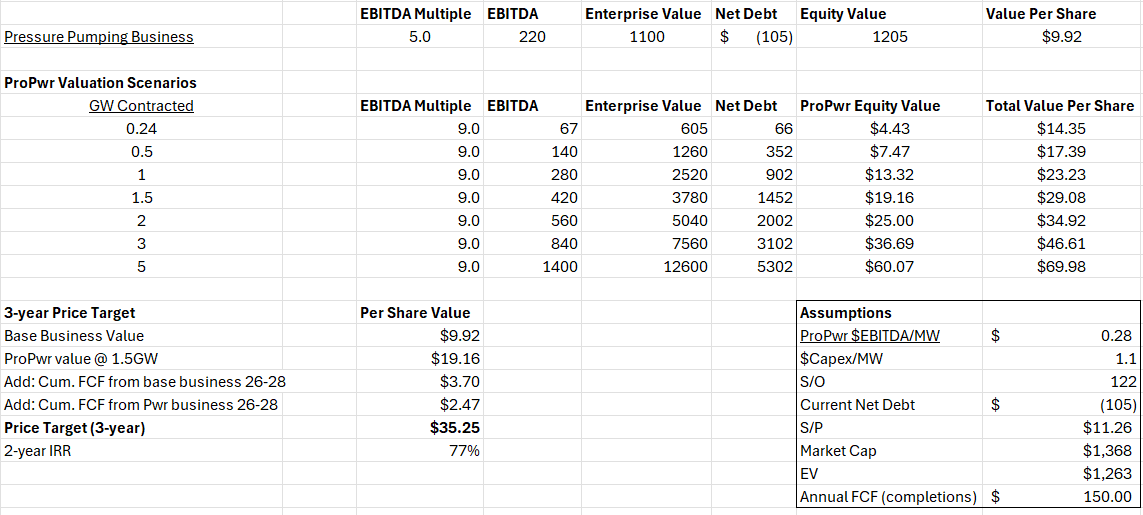

Below is a quick and dirty SOTP on my 3-year price target. Here are some key points to consider:

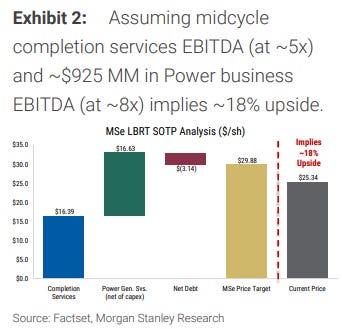

Multiple of ProPwr: I use 9x EBITDA for the multiple. Some will probably pushback here but this is my explanation: I think there are three suitable peer groups - Data Centers, IPPs and Contract Gas Compression. Data Center companies trade at >20x, IPPs at ~12-13x and contract compression at 9.5x (AROC/KGS). I believe that BTM power should trade higher than contract compression due to (1) better structural growth prospects with less cyclicality, (2) longer-term contracts (contract compression has ~3-4year contracts v.s. power which could stretch 10 years plus). So somewhere between 9.5x and 12-13x seems fair to me. 9x seems right if we see contract terms stretch to 7-10years. JPM is currently using 8x for LBRT’s business. KGS just bought a Permian Power player (~20% of its fleet with a data center) for 7.5x EBITDA, as a floor.

Multiple of Base Business: The stock has historically traded ~4-5x EBITDA. The street values LBRT’s pressure pumping business at 5.25x EBITDA in its SOTP. I use 5x given it’s a very similar business and EBITDA is currently recovering from trough levels. It doesn’t move the ultimate dial all too much anyways.

Add-back of cash generation: I add back $150m/year of FCF from the completions business and a cumulative $300m of cashflow that the power business would generate if it hits planned timelines over 2026-28. Given that we are subtracting the debt for equipment purchases we ought to credit cash generated also.

A key point of the thesis is that the completions business trades at a single-digit FCF multiple because the market hates the business, but if you can take that cash and deploy it to a high-multiple business then suddenly that cashflow is worth a lot.

2-year target: LBRT anaylsts are valuing the stock based on its end-of-2028 3GW deployment target (see below) and applying a ~8x multiple to it. LBRT stock price largely reflects this today. They have only contracted ~750MW so far (zero deployed). To be clear, 3GW is a target - not a contracted number. I value PUMP on a 2-year-view (Jan 2028) which would be looking at end-of-2030 1.5GW deployment for PUMP. So PUMP will deploy 1.5GW by 2030 (can be easily viewed as conservative given that at the current first-year run-rate they’ll hit 1.4GW), discounted back to a Jan 2028 PT just as the LBRT valuation is an end-of-2028 target discounted back to Jan 2026.

ProPetro is perhaps the most asymetric opportunity I’ve found in public markets with serious trading liquidity.

Catalyst

Another Data Center contract. Either an extension of the existing one or a new one of large size. I expect one in 2026.

The stock could be range bound until we get the contract. It may also run up into it like LBRT did. Either way, over 2 years, I am very confident that we will sign some more Data Centers. If we don’t, I don’t think I’ll lose money.

Appendix

JPM’s LBRT SOTP valuation:

Great write up, thoroughly enjoyed the read! Quick question though, your FCF floor analysis assumes trough Permian conditions, but the EIA, Goldman, and JPM are all forecasting WTI averaging $52-58 in 2026, below Permian breakeven. At $55 WTI with 8-9 fleets running, your completions FCF could be $20-60M, not $150M+. Do you think the downside protection argument can still hold at those oil prices, and how does that change the ProPwr funding flywheel?

Hey I js came across your substack, really enjoyed reading this write up, its genuinely authentic work you put in it. Thanks for sharing it.